Following the advice of the IMF in its document “FISCAL ADJUSTMENT

STRATEGY AND MEASURES TO PROTECT LOW-INCOME HOUSEHOLDS”

of February 2006, the Ministry of Finance decided to apply some of its

recommendations in the reform of our tax system. The IMF, in its standard

application in most countries, usually argues in favor of streamlining the tax

expenditures or tax concessions.

They believe that “tax concessions generally have

good intentions of promoting jobs and growth, but they effectively result in

discriminatory higher tax rates for those who are not intended to benefit from the

concessions. These results in an inefficient allocation of resources by promoting

unproductive investment whose main purpose may be to take advantage of these

incentives. As a consequence, relative incentives are distorted and government

revenues are reduced.”

The IMF had estimated that the tax concessions in the individual income to be

around 40 percent of the revenue actually collected, or 0.6 percent of GDP. Salaried

employees, in the PAYE system, are the main beneficiaries of these concessions.

Likewise, deductions for alimony and maintenance, for medical expenses and for

donations to charitable institutions are not considered as tax expenditures. The

deductions considered as tax expenditures were: Retirement pension relief. - a

deduction enjoyed by salaried employees only, with a maximum, in 2004/05, of Rs

75,000. Emoluments relief. - a deduction, enjoyed by salaried employees only, of 15

percent of gross income with a maximum, in 2004/05, of Rs 125,000.; Pension

contribution- contributions to approved superannuation/pension funds or schemes are

deductible. Interest relief. - a deduction of interest paid on loans for the purchase of a

house or financing of tertiary education of dependent children. Investment relief- A

deduction of 40 percent of shares bought in the Stock Exchange, or authorized mutual

funds; or investments in newly issued securities of an investment trust company. The

maximum allowable is, in 2004/05, Rs 50,000 and any excess over this amount shall

be deductible in two succeeding income years- Relief for life insurance premium.

The amount of life insurance premium payable under a policy on the taxpayer’s life,

the life of the dependent spouse, or any children under 18 years of age is deductible.

Saving relief. - the deduction of the contributions payable to a personal pension

scheme, the contributions payable under an approved annuity contract to provide for a

life annuity during old age, and the contributions payable under a scheme to provide

medical and ambulance services.

But the IMF had recommended that since the salaried employees are

discriminated against vis a vis self-employed workers, there are grounds to maintain

the tax expenditures in the individual income tax until the tax administration reforms

make it feasible to bring all workers (including the self-employed) into the tax net.

The MOF did not wait for such tax administration reforms; it chose to go in

drastically for the complete removal of tax expenditures and some non-tax

expenditures in the 2006/07 budget.

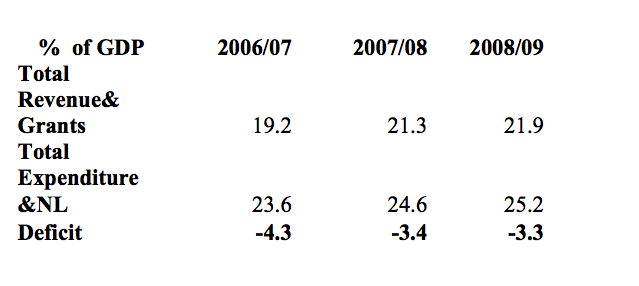

As a result the MOF will be collecting some extra Rs 4 billion in taxes in FY

08/09 and an extra Rs 9 billion in terms of total revenue and grants. Over the 2005/06

figures, tax revenue in FY 08/09 are expected to show a boon of Rs15 billion whereas

total revenue and grants are expected to increase by 22 billion .Total expenditure and

net lending will however increase by 21.3 billion. The budget deficit has been reduced

by maintaining a relatively low capital expenditure without any meaningful effort to

reduce recurrent expenditure and wastage and by increasing the tax burden on the

population and creating doubtful funds outside the budget- a practice that has often

been criticised by the IMF. On the expenditure side, the IMF had recommended “a

sharp reduction in poorly targeted transfers and subsidies, accompanied by a

moderate increase in capital expenditures in priority sectors, including energy,

transportation, ports, and telecommunication. Capital spending increase would

include the spending on retraining workers in non-priority “sunset” industries with a

view of shifting them to priority “sunrise” industries and would possibly be financed

by external grants.” It has been much easier to tax and much more difficult to reduce

redundant expenditures and boost priority capital expenditures.

We are thus not surprised that a study carried out by the Ms Kumari Juddoo & others

from the University of Mauritius-The Impact of the Tax Reform on the Individual

Income Tax System – has found that

-

New tax regime being simple has not been able to achieve the other main

canons of a good tax system – fairness (based on ability to pay) and equitable

(decrease tax distortions for the couple)

-

New tax regime has eliminated all tax planning possible by taxpayers for a

better quality of life

-

Taxpayers earning more than Rs 25,000 especially the middle income earner

having a relatively higher burden of the new tax

-

Inequality increases slightly with the imposition of the new tax regime except

for the taxpayers with more than three dependents where the Gini coefficient

decreases slightly.

-

Previous regime shows sign of progressivity, taking a greater share from high-

income earners and a smaller share from low-income earners – Income

distribution more equal

Post tax Gini Coefficient

No

Dependent

|

1

Dependents

|

2

Dependents

|

3 or more

dependents

|

|

Monthly Gross

Income

|

0.234

|

0.412

|

0.371

|

0.355

|

Monthly

Disposable

Income

|

0.242

|

0.415

|

0.378

|

0.352

|

This report of the UOM in a way concludes that the tax reform was not anchored

in Mauritian realities; it was another blind application of IMF prescriptions that

are usually applied to all developing and emerging market countries; and the MOF

as a good student applied these to the letter. The report is categorical that the

previous system was better and that it should be reintroduced with

-

some new savings scheme within the tax system to enable economy growth and encourage better future quality of life;

-

some savings scheme within the tax system to encourage taxpayers to plan for a better future. There are many households who are dipping deep into their assets and savings to ensure a better human capital formation of world standards for the country. These expenses are not liable for deduction under the new tax system despite the fact that Government has failed to provide to these households the necessary institutions of learning in fields of medicine, engineering, computer science –you name it- that meet minimum global standards.

-

the deduction for donations to charity and as such many of those NGOs are facing financial crisis as they were heavily dependent on such donations.

-

a new Income Deduction Threshold to alleviate the taxpayers not liable to tax prior to publication PRB Report and

-

the compulsory pension contribution tax deductible to reduce the burden on taxpayersThe reduction in of the corporate tax rate to 15% had gifted millions of rupees to big enterprises and banks; now we see that the high income earner is also benefiting from the income tax reform; that’s what we have been always saying-the reforms imposed by the Bretton Woods Institutions, including the new employment legislation, that has now given the private sector a free hand to fire workers, have mostly benefited “les grands patrons”

High Income Earner

|

Old

|

New

|

Rs

|

Rs

|

|

Salary

|

3,250,000

|

3,250,000

|

Emoluments relief (15%)

|

(135,000)

|

|

Personal allowance

|

(85,000)

|

|

Dependent Children

|

(60,000)

|

|

Dependent Spouse

|

(60,000)

|

|

Interest relief

|

(250,000)

|

|

Savings relief

|

(650000)

|

|

Insurance premium

|

(80,,000)

|

(415,000)

|

Income exemption

threshold

|

1,930,000

|

2,835,000

|

Chargeable income

|

||

Tax liability

|

||

10%

|

2,500

|

|

15%

|

425,250

|

|

20%

|

5,000

|

|

25%

|

470,000

|

|

TOTAL tax paid

|

477,500

|

425,250

|

Effective tax rate

|

14.7

|

13.1

|

Middle Income

Earner

|

Old

|

New

|

Rs

|

Rs

|

|

Salary

|

650,000

|

650,000

|

Emoluments relief(15%)

|

(97,500)

|

|

Personal allowance

|

(85,000)

|

|

Dependent Children

|

(60,000)

|

|

Dependent Spouse

|

(60,000)

|

|

Interest relief

|

(250,000)

|

|

Savings relief

|

(130,000)

|

|

Insurance premium

|

(80,,000)

|

(415,000)

|

Income exemption

threshold

|

112,500

|

235,000

|

Chargeable income

|

||

Tax liability

|

||

10%

|

||

15%

|

35,250

|

|

20%

|

||

25%

|

||

TOTAL tax paid

|

35,250

|

|

Effective tax rate

|

0.0

|

5.4

|